Why Is My Hurricane Claim Taking So Long in Louisiana?

Filed Your Hurricane Claim Weeks Ago and Still Waiting? Here’s Why It Might Be Delayed

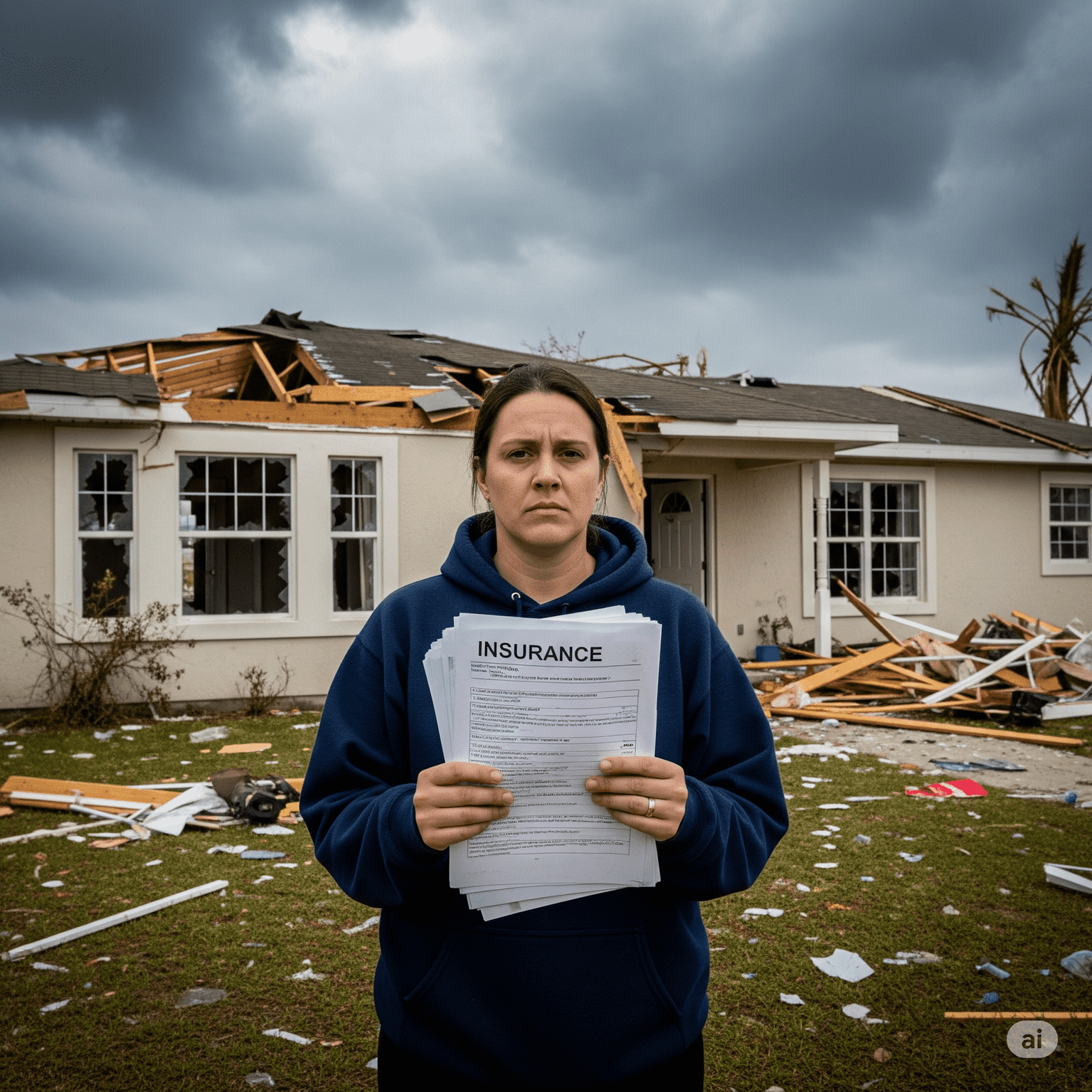

Weeks, months, or even a year after the storm, you’re still waiting. Your home in Louisiana is damaged, your life is on hold, and the insurance company you paid for protection is silent. The initial shock of the hurricane has been replaced by a slow-burning frustration as you ask a question no policyholder should have to ask: Why is my claim taking so long?

While a certain amount of processing time is expected after a major disaster, prolonged and unexplained delays are often a strategic move by the insurer. If you’re wondering why hurricane claim taking so long Louisiana, understanding the difference between a legitimate delay and a deliberate stall tactic is the key to fighting back and getting the money you need to rebuild.

You are not powerless in this situation. The attorneys in the Bloom Legal Network specialize in breaking through these delays and holding insurance companies accountable for what they owe.

Legitimate Reasons vs. Unacceptable Excuses

Not every delay is a sign of malice. After a catastrophic hurricane hits Southeast Louisiana, the entire system is overwhelmed. It’s important to recognize what is a reasonable bottleneck versus what is an unacceptable excuse.

Potentially Legitimate Reasons for Initial Delays:

- Widespread Devastation: When a storm impacts a huge area from New Orleans to the Florida Parishes, thousands of claims are filed at once. Insurers are swamped, and it can take time to get to everyone.

- Adjuster Shortage: Insurers often bring in adjusters from out of state who are not only overloaded with cases but are also unfamiliar with Louisiana’s specific building codes and repair costs, leading to slower, often inaccurate, assessments.

- Complex Damage: If your home in Jefferson Parish has a complex combination of wind, flood, and structural damage, the investigation will naturally take longer than a simple roof claim.

However, these legitimate reasons have a shelf life. An initial delay of a few weeks can be understandable. A delay of many months with no clear communication is a major red flag.

Red Flags: Is Your Insurer Stalling on Purpose?

Prolonged delays are often a sign of an insurer acting in “bad faith.” They hope that if they drag the process out long enough, you’ll either give up or accept a lowball offer out of sheer desperation.

Here are common delay tactics to watch for:

- The Endless Document Loop: The adjuster repeatedly asks for documents or photos you have already sent. This is a classic trick to bog down the process and blame you for the delay.

- Radio Silence: Your calls and emails to the adjuster go unanswered for weeks on end. A complete lack of communication is unprofessional and a strong indicator of bad faith.

- The Adjuster Shuffle: Your claim is passed from one adjuster to another, forcing you to retell your story and start from scratch each time. This is a deliberate way to create confusion and avoid accountability.

- Demanding Unnecessary Information: The insurer requests irrelevant information (like your personal credit history) that has no bearing on your property damage claim.

- Vague and Evasive Answers: When you do get a response, it’s non-committal and gives you no clear timeline or explanation for the delay.

If these tactics sound familiar, your insurer is likely not dealing with you fairly. Louisiana law protects you from this behavior, and you should immediately seek legal guidance. Contact Bloom Legal Network to spot and fight these bad faith tactics.

Your Rights Under Louisiana Law

You have more power than you think. Louisiana has specific laws in place to protect policyholders from unreasonable delays by insurance companies.

The two most important are:

- La. R.S. 22:1892: This statute requires an insurer to pay any undisputed amount of a claim within 30 days of receiving “satisfactory proof of loss” from the policyholder. A “satisfactory proof of loss” is simply enough information to show the extent of your damages.

- La. R.S. 22:1973: This law outlines an insurer’s duty of “good faith and fair dealing.” It explicitly prohibits them from failing to pay a claim within 60 days after receiving satisfactory proof of loss when that failure is arbitrary, capricious, or without probable cause.

When an insurer violates these statutes, they can be forced to pay not only your original claim but also significant penalties and your attorney’s fees.

These laws are your leverage. An experienced attorney can use them to force the insurance company to act. Let Bloom Legal Network connect you with a legal professional in the Metairie or St. Tammany Parish area who can assert your rights.

How an Attorney Can Break the Logjam

A phone call from a frustrated homeowner can be easily ignored by an insurance company. A formal demand letter from a law firm cannot. Hiring an attorney sends a clear signal that you will not be pushed around.

An attorney can take immediate action to:

- Send a Formal Demand Letter: This letter will outline the insurer’s violations and demand payment within the statutory deadlines, officially starting the clock on potential penalties.

- Stop the Stall Tactics: A lawyer will take over all communications, preventing the insurer from using their usual tricks on you.

- Leverage the Threat of Litigation: Insurers know that a bad faith lawsuit can be incredibly costly for them. The credible threat of a lawsuit is often enough to get them to stop delaying and start negotiating fairly.

- File a Lawsuit: If the insurer still refuses to pay what you’re owed, your attorney can file a lawsuit to recover your damages, bad faith penalties, and legal fees.

You have been patient long enough. While your life is in limbo, your insurer’s profits are not. It’s time to take control of your claim.

📞 Call 504-599-9997 📧 Send an email to info@bloomlegal.com

Don’t let your insurance company dictate your future. Contact Bloom Legal Network today to be matched with a dedicated legal advocate who will fight to get your claim paid without delay.

Frequently Asked Questions

While some initial delays can be expected after a widespread disaster due to the sheer volume of claims, prolonged and unexplained delays are often a red flag. Legitimate reasons for a delay can include an adjuster shortage or complex damage assessments. However, if your insurance company is repeatedly asking for documents you’ve already sent, ignoring your calls and emails, or constantly shuffling your claim between different adjusters, they may be acting in “bad faith” and hoping you’ll give up or accept a low offer.

Louisiana law provides specific protections for policyholders. Under La. R.S. 22:1892, insurers are required to pay any undisputed amount of a claim within 30 days of receiving “satisfactory proof of loss.” Additionally, La. R.S. 22:1973 outlines the insurer’s duty of “good faith and fair dealing” and prohibits them from arbitrarily failing to pay a claim within 60 days after receiving proof of loss. If an insurer violates these statutes, they can be held liable for significant penalties and your attorney’s fees in addition to the original claim amount.

If you’ve been waiting for months with little to no communication, suspect your insurer is using stall tactics, or feel like you’re being pushed around, it’s time to seek legal help. An attorney can send a formal demand letter to the insurer, take over all communication to stop the stall tactics, and use the threat of a bad faith lawsuit to compel the company to act. Having a legal professional on your side sends a strong message that you will not be ignored and are serious about getting the money you need to rebuild.