Commercial Roof Damage Claim: Why Insurance Companies Underpay and How to Fight Back

My commercial roof was damaged in a Louisiana hurricane – why is my insurance check so low?

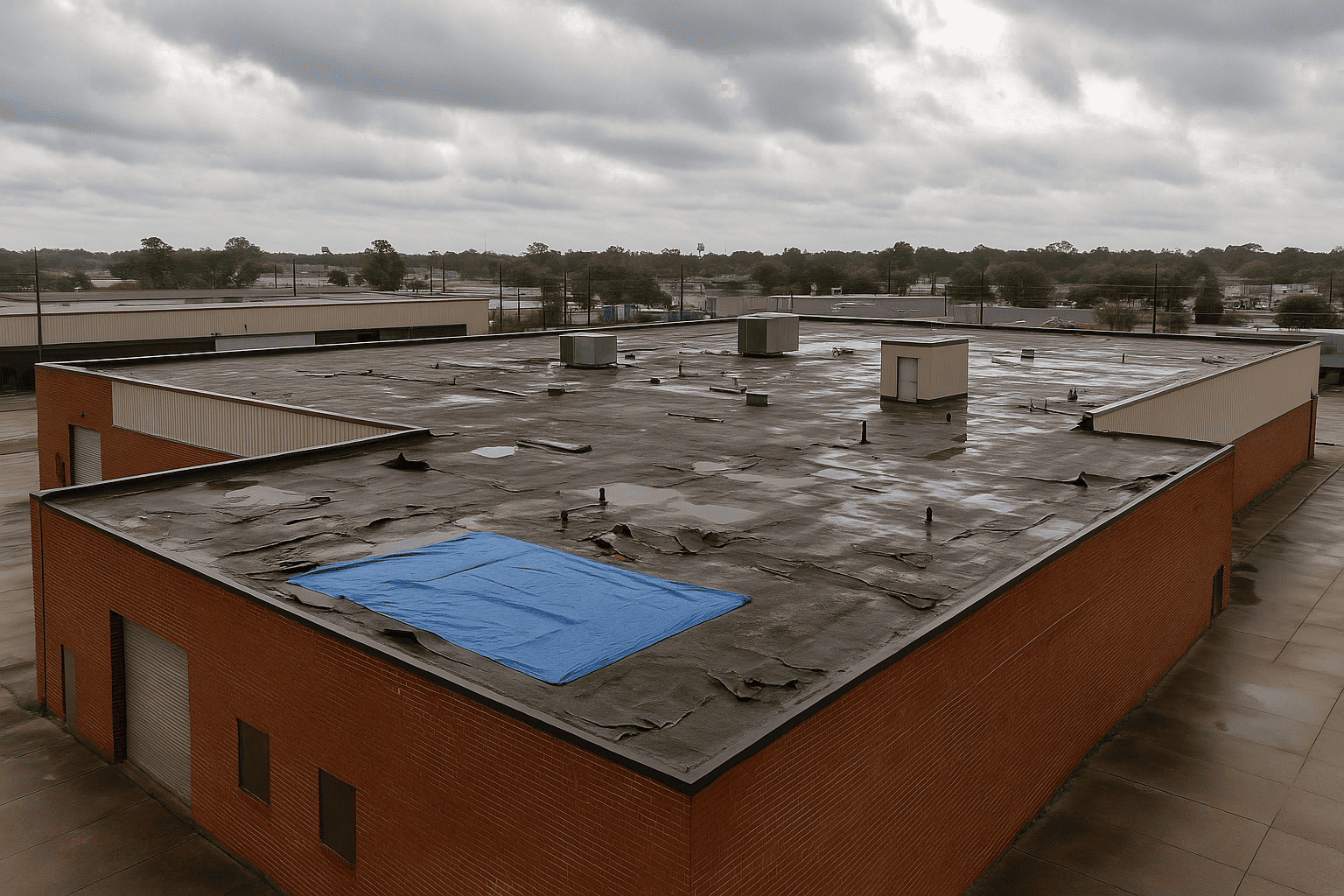

In Louisiana, where hurricanes and tropical storms are a recurring threat, commercial property owners know that roof damage is often the first and most expensive issue to deal with after a storm. Major storms can bring strong winds and high winds, which frequently cause wind damage to commercial roofs by dislodging roofing materials, flashing, vents, and membranes.

But here’s the problem: insurance companies routinely underpay roof damage claims, especially after widespread disasters. This underpayment can create a significant financial burden for property owners and businesses, leaving them responsible for unexpected repair costs.

If you don’t catch it early or push back strategically, you may end up footing the bill for repairs that should have been covered. The insurance company’s handling of your claim and your understanding of your property insurance policy are critical in these situations.

Here’s why insurers lowball roof claims, and what you can do to protect your business and fight back. Having the right commercial property insurance and insurance coverage is essential to mitigate risks and ensure your property is adequately protected.

Why Roof Claims Are Often Underpaid in Louisiana

1. Hidden Damage Is Easy to Overlook

Hurricanes don’t always rip off shingles or cave in the roof visibly. Instead, they often cause damage to:

- Flashing and membrane systems

- Underlayment and decking

- Fasteners and structural components

- HVAC and drainage systems on flat roofs

Insurers may perform a cursory inspection and declare “minimal damage”, while missing long-term vulnerabilities that lead to water intrusion and mold months later.

2. Insurers Use Biased or Inexperienced Inspectors

After a storm in Southeast Louisiana, insurers often bring in out-of-state adjusters who:

- Lack of experience with commercial roofing systems

- Miss subtle or structural damage

- Rely on software to generate estimates without expert verification

This leads to drastically underestimated repair costs, especially in larger commercial buildings across St. Tammany Parish and St. Charles Parish.

3. Roof Age Is Used as a Justification for Depreciation

Insurance companies love to point out that your roof is “old”, even if it was properly maintained. They may:

- Apply aggressive depreciation to your payout

- Recommend partial repair instead of full replacement

- Claim the damage was pre-existing or due to wear-and-tear

When calculating your payout, insurers may use actual cash, actual cash value (ACV), or replacement cost value (RCV). Actual cash and actual cash value account for depreciation, often resulting in lower settlements, while replacement cost value pays for the cost to replace the damaged property without deducting for depreciation. Even a properly maintained roof can be severely damaged by hurricane-force winds, so age should not be a blanket excuse to underpay.

Insurers often rely on the specific policy language in your insurance policy or reference terms in their insurance policies to justify underpayment or denial of claims.

Bloom Legal Network can connect you with a property damage lawyer who knows how to challenge these tactics and get your full repair costs recognized.

Signs You’re Being Underpaid for Commercial Roof Damage

If your insurance offer doesn’t match the reality of your damage, pay attention to red flags like:

- Payouts that don’t include full tear-off and replacement

- No line items for underlayment, decking, or roof vents

- Denials of interior water damage as “not roof-related”

- Denied claims based on the roof’s age alone

- Filing multiple claims or a roof damage insurance claim within a short period, which can signal higher risk to insurers and may result in premium increases or policy scrutiny

Each insurance claim should be carefully reviewed to ensure all damages are included.

Own a commercial property in New Orleans or Jefferson Parish? Don’t take the first check as the final word. Let a legal expert review the offer before you cash it, it could be thousands (or tens of thousands) too low. Understanding the claim process and claims process for insurance claims is crucial—having paid your premiums means you are entitled to a fair settlement.

What Your Roof Claim Should Actually Cover

A properly submitted and documented roof damage claim should account for:

- Full replacement cost, including materials, labor, and code upgrades

- Interior damage caused by leaks (ceilings, drywall, flooring, equipment)

- Tarping, mitigation, and temporary repairs such as emergency repairs, immediate repairs, and permanent repairs to address the damaged roof

- Covering the damaged area to prevent further issues until permanent repairs are completed

- HVAC and equipment damage on rooftops

- Lost income if the damage forced you to close operations

- Extra expenses and, for some policies, additional living expenses if the property is uninhabitable

Coverage should address all business property affected by the covered event and include the process of repairing the roof. The insurer’s job is to restore your property to pre-loss condition, not cut corners or push cheaper alternatives.

How to Strengthen Your Roof Damage Claim

1. Get a Licensed Roofer or Engineer to Inspect the Damage

Don’t rely solely on the insurance adjuster. A roofer familiar with hurricane damage in Southeast Louisiana can:

- Identify hidden and structural damage

- Provide detailed replacement cost estimates

- Test moisture levels under the roof deck

2. Preserve Evidence

Take clear photos and videos of:

- Exterior and interior damage

- Water stains, ceiling collapse, or mold

- Any repairs or mitigation you’ve done

Keep receipts for tarps, patchwork, or temporary closures. Document all steps you take to prevent further damage, such as covering exposed areas, making emergency repairs, or immediate repairs. This helps show you acted to mitigate loss while your claim is processed.

3. Don’t Sign a Quick Settlement

Many insurers will offer fast but low settlements hoping you’ll move on. Signing that check may waive your right to pursue additional compensation later.

Not sure if the offer is fair? Call Bloom Legal Network before you sign anything. We’ll connect you with a Louisiana insurance lawyer who can assess your claim.

When to Call a Property Damage Attorney

If you’re dealing with any of the following, it’s time to bring in legal support:

- Denied or delayed roof claim

- Offer that’s far below contractor estimates

- Insurer refuses to cover full replacement

- Disagreements about cause of damage (e.g., wind vs. wear)

Our attorney has extensive experience handling commercial roof damage claims and disputes, ensuring clients receive knowledgeable guidance throughout the process.

Roof claims are among the most technically complex, and insurers know that many property owners won’t have the time, expertise, or energy to push back. But legal advocacy levels the playing field.

Don’t Let Your Roof Claim Collapse Under Pressure

Your commercial roof protects your entire investment. Don’t let insurers chip away at your recovery with vague language, rushed inspections, or underpriced estimates.

If your business took roof damage during hurricane season, whether in downtown New Orleans or on the outskirts of Slidell, make sure you know your rights, document your losses, and take action before it’s too late.

📞 Call Bloom Legal Network at 504-599-9997

📧 Email info@bloomlegal.com

We’ll connect you with a Louisiana insurance attorney who will fight for the roof claim you actually deserve.

Frequently Asked Questions

1. Why is my insurance payout for commercial roof damage so low after a Louisiana hurricane?

Insurance companies may underpay commercial roof claims for a few key reasons. They might use inexperienced or out-of-state adjusters who miss subtle or structural damage, especially on complex commercial systems. Insurers may also apply aggressive depreciation based on the roof’s age, even if a hurricane caused severe damage. Finally, a cursory inspection might overlook hidden damage to flashing, underlayment, or structural components that can lead to bigger problems later on.

2. What are the signs that my insurance company is underpaying my commercial roof damage claim?

Red flags that indicate you’re being underpaid include an offer that doesn’t cover full tear-off and replacement, a settlement that omits line items for underlayment or decking, a denial of interior water damage, or a claim denial based solely on the roof’s age. If your insurance payout is significantly lower than a licensed roofer’s estimate, it’s a strong sign the offer may be too low.

3. What can I do to fight back against a low insurance settlement for my commercial roof damage?

To strengthen your claim, you should first get a detailed inspection and estimate from a licensed roofer or engineer who is experienced with hurricane damage in your area. Document everything by taking photos and videos of both exterior and interior damage. It’s also crucial not to sign a quick settlement check, as this may waive your right to seek additional compensation later. If your claim is denied or the offer is far below your contractor’s estimate, it may be time to consult with a property damage attorney.